Leave Travel Concession (LTC) Cash Voucher Scheme for Central Govt Employees

Finance Ministry Order on LTC Cash Vouchers Scheme – PDF Download

The Department of Expenditure published an important order on 12th October 2020 regarding the new LTC scheme for Central Government employees.

F.No.12(2) /2020-EII(A)

Ministry of Finance

Department of Expenditure

EN(A) Branch

North Block, New Delhi

12th October 2020

Office Memorandum

Sub: Special cash package equivalent in lieu of Leave Travel Concession Fare for Central Government Employees during the Block 2018-21.

In view of the Covid-19 pandemic and resultant nationwide lockdown as well as disruption of transport and hospitality sector, as also the need for observing social distancing, a number of Central Government employees are not in a position to avail themselves of LTC for travel to any place in India or their Hometowns in the current Block of 2018-21.

2. With a view to compensate and incentivise consumption by Central Government employees thereby giving a boost to consumption expenditure, it has been decided that cash equivalent of LTC, comprising Leave Encashment and LTC fare of the entitled LTC may be paid by way of reimbursement if an employee opts for this in lieu of one LTC in the Block of 2018-21 subject to the following conditions:-

a) The employee spends the money of a larger sum than the entitlement on account of LTC on actual expenditure.

b) Cash equivalent of full leave encashment will be allowed, provided the employee spends an equal sum. This will be counted towards the number of leave encashment on LTC available to an employee.

C) The deemed LTC fare for this purpose is given below:-

|

Category of employees |

Deemed LTC fare per person |

|

Employees who are entitled to business class of airfare |

Rs. 36,000 |

|

Employees who are entitled to economy class of airfare |

Rs. 20,000 |

|

Employees who are entitled to Rail fare of any class |

Rs. 6,000 |

d) The cash equivalent may be allowed if the employee spends a sum 3 times of the value of the fare given above.

e) The amount both on account of leave encashment and fare shall be admissible if the employee spends (i) an amount equal to the value of leave encashment and; (ii) an amount 3 times of the cash equivalent of deemed fare, as given above on purchase of such items/availing of such services which carry a GST rate of not less than 12% from GST registered vendors/service providers through digital mode and obtains a voucher indicating the GST number and the amount of GST paid.

f) The admissible payment shall be restricted to the full value of the package [leave encashment as admissible for LTC and deemed fare] or depending upon the spending as per example given at Annexure-A.

g) While TDS is applicable in the case of leave encashment, since the cash reimbursement of LTC fare is in lieu of deemed actual travel, the same shall be allowed exemption on the lines of existing income-tax exemption available to LTC fare. The legislative amendment to the provisions of the Income-Tax Act, 1961 for this purpose shall be proposed in the due course. Hence, TDS shall not be required to be deducted on the reimbursement of deemed LTC fare.

3. Head of the Departments / DDOs may make reimbursement under this package as per the details given above on receipt of invoices of purchases made / services availed during the period post the issuance of this order from the employees who are desirous to avail this package. It may be noted that in order to avail this package an employee should opt for both leave encashment and LTC fare.

4. An amount up to 100% of leave encashment and 50% of the value of deemed fare may be paid as advance into the bank account of the employee which shall be settled based on production of receipts towards purchase and availing of goods and services as given in Para 2(e). The claims under this package (with or without advance) are to be made and settled within the current financial year. Non-utilization / under-utilization of advance is to be accounted for by the DDOs in accordance with the extant provisions relating to LTC advance i.e. immediate recovery of full advance in the case of non-utilization and recovery of unutilized portion of the advance with penal interest.

5. These orders will take effect from the date of issuance of this Office Memorandum and will be in force during the current financial year till 31st March 2021.

6. All the Ministries/Departments are requested to bring the contents of this OM to the notice of all its Attached and Subordinate offices for their information.

Hindi version of this Office Memorandum will follow.

sd/-

(B.K.Manthan)

Deputy Secretary to the Govt. of India

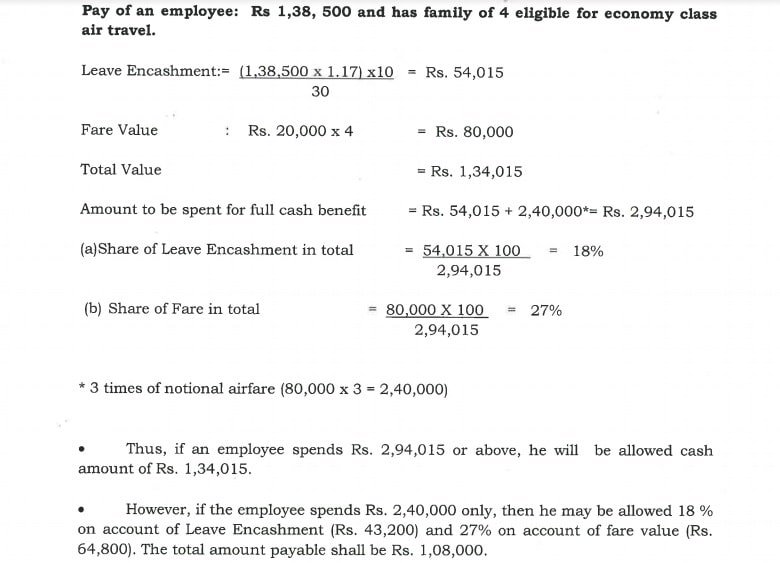

Example:

Pay of an employee: Rs 1,38, 500 and has family of 4 eligible for economy class air travel.

Leave encashment (1,38,500 x 1.17) x10/30 = Rs. 54,015

Fare Value: Rs. 20,000 x 4 = Rs. 80,000

Total Value: = Rs. 1,34,015

Amount to be spent for full cash benefit = Rs. 54,015 + 2,40,000*= Rs. 2,94,015

(a) Share of Leave Encashment in total = 54,015 X 100 / 2,94,015 = 18%

(b) Share of Fare in total = 80,000 X 100 / 2,94,015 = 27%

* 3 times of notional airfare (80,000 x 3 = 2,40,000)

- Thus, if an employee spends Rs. 2,94,015 or above, he will be allowed cash amount of Rs. 1,34,015.

- However, if the employee spends Rs. 2,40,000 only, then he may be allowed 18 % on account of Leave Encashment (Rs. 43,200) and 27% on account of fare value (Rs. 64,800). The total amount payable shall be Rs. 1,08,000.

Click to view the Finmin Order dated 12.10.2020

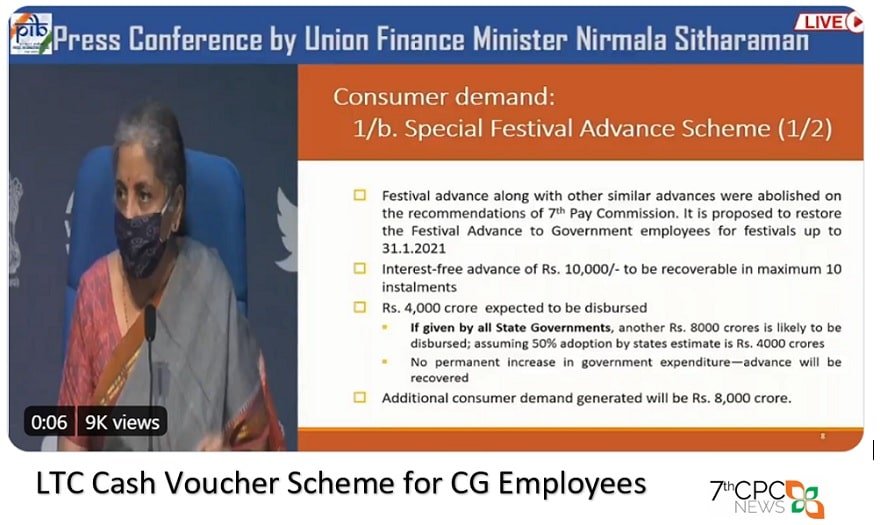

Special Festival Advance Scheme

Special Festival Advance Scheme for non-gazetted employees is being revived as a one-time measure, for gazetted employees too. All central govt. employees can now get an interest-free advance of Rs.10,000, in the form of a prepaid RuPay Card, to be spent by March 31, 2021

Special Festival Advance Scheme is being revived as a one-time measure. All central govt. employees can now get an interest-free advance of Rs. 10,000, recoverable in maximum 10 installments: Finance Minister

The interest-free advance of Rs 10,000 under the Special Festival Advance Scheme to be paid back in 10 installments.

The one-time disbursement of the Special Festival Advance Scheme is expected to amount to ₹4,000 crores; if given by all state governments, another ₹8,000 crores is expected to be disbursed. Employees can spend this on any festival.

Employees will get a pre-loaded Rupay Card of the advance value

Under LTC Cash Voucher Scheme, government employees can opt to receive cash amounting to leave encashment plus 3 times the ticket fare, to buy items that attract GST of 12% or more. Only digital transactions allowed, GST invoice to be produced, said Sitharaman.

Special Cash Package on LTC Calculator 2020

A simple online calculator for finding the maximum amount to avail complete cash benefit from this Special Cash Package Scheme on Leave Travel Concession. [Click to calculate]