IRCTC News : GST on Catering Services

Applicability of Goods and Service Tax (GST) on Catering Services

GOVERNMENT OF INDIA

MINISTRY OF RAILWAYS

(RAILWAY BOARD)

No.2012/TG.III/631/2

New Delhi dated 29.06.2017

The General Managers

All Indian Railways

The CMD/IRCTC

New Delhi

CMD/KRCL,

Navi Mumbai

(Commercial Circular No.44 of 2017)

Sub: Applicability of Goods and Service Tax (GST) on Catering Services

The issue of implementation of Goods and Service Tax (GST) on Catering Services on Indian Railways has been examined in consultation of Finance Commercial Dte. of Railway Board. Accordingly, following are advised:-

1. The chargeable GST on catering services on railways is as under:-

(i) For static units not having facility of air conditioning or central heating at any time during the year- 12% with full Input Tax Credit (ITC)

(ii) For static units having facility of air conditioning or central heating at any time during the year-18% with full Input Tax Credit (ITC)

(iii) For Rajdhani/Shatabdi/Duronto and other Mail/Express trains -18% with full Input Tax Credit (ITC)

2. The above GST on catering charges is applicable w.e.f 01.07.2017.

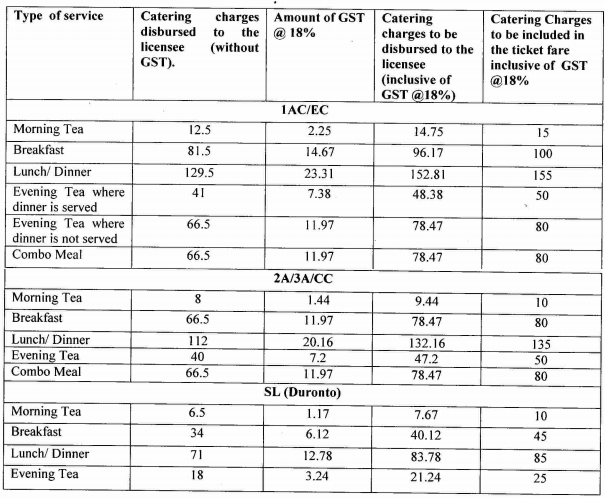

3. The revised catering apportionment charges for Rajdhani/Shatabdi/Duronto trains and other similar type of Rajdhani trains where catering charges are inbuilt in ticket fare are as under:-

4. In case of Rajdhani/Shatabdi/Duronto type trains where catering charges are part of the ticket fare, amount of GST is to be reimbursed to the service providers on submission of proof of deposit of the same with the appropriate Government Authority. However, in case of Mail/Express trains and other static units where catering services are provided on payment basis and the above taxes are collected directly from the passengers through cash memo, money receipts etc., Zonal railways /IRCTC shall ensure that the GST collect from the passenger are deposited with the concerned Authorities as per the guidelines /procedures laid down by the M/o Finance. To ensure the same zonal railways shall also obtain monthly proof of compliance of tax deposit by the service provides as per laid down procedures.

5. In case of other mail/express trains and static unit, the GST amount shall not be rounded off. In case of showing separate GST amount for CGST and SGST/UTGST in that case also GST amount shall be separately mentioned upto two decimal place. As regard rounding off of chargeable amount, after levy of GST on the total amount it shall be rounded off to the nearest rupee.

6. In addition to the above, GST on catering services of other premium trains like Tejas, Gatiman, Shivalik etc. shall be levied @ 18%. Accordingly, necessary changes in the catering apportionment charges shall be advised by the Zonal Railways to CRIS.

This issue with the concurrence of Finance Dte. of Railway Board.

Please acknowledge receipt of this letter.

sd/-

(Smita Rawat)

Exe. Director (T&C)

Railway Board