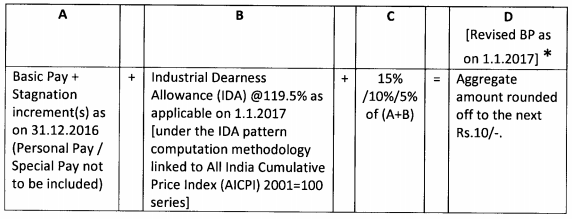

3rd Pay Revision for CPSE : Fitment Benefit as per OM dated 3.8.2017

Fitment Benefit

(i) In case additional financial impact in the year of implementing the revised pay-package of a CPSE is within 20% of average PBT of last 3 years, a uniform full fitment benefit of 15% would be provided.

Also Check: 3rd Pay Revision for CPSE : Implementation order issued by DPE on 3.8.2017

(ii) If the additional financial impact in the year of implementing the revised pay-package is more than 20% of the average PBT of last 3 Financial Years (FYs), then the revised pay-package with recommended fitment benefit of 15% of BP+DA should not be implemented in full but only partly, as per the part-stages recommended below:-

| Part stages | Additional financial impact of the full revised pay package as a % of average PBT of last 3 FYs | Fitment benefit (% of BP+DA) |

| I | More than 20% but upto 30% of average PBT of last 3 FYs | 10% |

| II | More than 30% but upto 40% of average PBT of last 3 FYs | 5% |

(iii) At the time of implementation of pay revision, if the additional financial impact after allowing full / part fitment exceeds 20% of the average PBT of last 3 years, then PRP payout / allowances should be reduced so as to restrict impact of pay revision within 20%.

(iv) Subsequent to implementation of pay revision, the profitability of a CPSE would be reviewed after every 3 years and

a) if there is improvement in the average PBT of the last 3 years, then full pay package/ higher stage of pay package would be implemented while ensuring that total additional impact (sum total of previously implemented part pay package and proposed additional package) stays within 20% of the average of PBT of last 3 years

b) if the profitability of a CPSE falls in such a way that the earlier pay revision now entails impact of more than 20% of average PBT of last 3 year, then PRP/ allowances will have to be reduced to bring down impact.

- 3rd Pay Revision for CPSE : FITMENT BENEFIT

- 3rd Pay Revision for CPSE : METHODOLOGY FOR PAY FIXATION

- 3rd Pay Revision for CPSE : INCREMENT

- 3rd Pay Revision for CPSE : DEARNESS ALLOWANCE

- 3rd Pay Revision for CPSE : HRA and HRR

- 3rd Pay Revision for CPSE : PERFORMANCE RELATED PAY (PRP)

- 3rd Pay Revision for CPSE : SUPERANNUATION BENEFITS

- 3rd Pay Revision for CPSE : LEAVE REGULATIONS/MANAGEMENT

- 3rd Pay Revision for CPSE : DATE OF IMPLEMENTATION AND PAYMENT OF ALLOWANCES